<< Hide Menu

1.2 Resource Allocation and Economic Systems

7 min read•june 18, 2024

Jeanne Stansak

dylan_black_2025

Jeanne Stansak

dylan_black_2025

Three Economic Questions

In every economy there are three questions that must be answered:

What goods and services will be produced?

Since scarcity exists, no society has the resources to produce everything that the people want, leading to this question. An economy has to decide what goods and services are most wanted and needed. For example, when an economy chooses between building or fixing roads, or buying textbooks for schools. This can also involve making decisions like whether the government should conserve wilderness areas or open them up for development. There are many debates over who answers this question. The different answers of who chooses what gets produced is part of what defines an economic system. For some, the answer is the market, where invisible forces defined by consumer and producer behavior drive market production, with price changes acting as the signal of over or underproduction. For others, the answer is a central system, such as the government. In this case, the government would decide what, and how much is produced.

How will goods and services be produced?

This question deals with how businesses and other producers should go about producing various goods and services. For example, asking whether pipes should be made out of copper or plastic, or whether clothing should be made by machines or made by hand. This question, one again, has many answers. This question is fundamental to our study of microeconomics, because we'll be directly observing the actions of firms and their various market structures. This question of economics tangentially asks how we set up our industries: does one firm run the entire market? or are there many smaller firms? How do they interact? These questions are a more microeconomic perspective on the question of how goods are produced.

For whom will the goods and services be produced?

This question is answered after the production of goods and services, as it is decided who should be allowed to consume the goods and services that have been produced. For example, should it be based on a first-come, first-served basis or based on whether the consumer can afford the goods or services? In microeconomics, we'll be looking at how consumers interact with firms and how firms interact with consumers. A firm may only sell to one type of consumer or charge different prices to different consumers.

What is an Economic System?

An economic system is a set of rules, institutions, and practices that determine how a society produces, distributes, and consumes goods and services. Every society must make choices about what goods and services to produce, how to produce them, and who will receive them. These choices are guided by an economic system, which can be thought of as the framework that a society uses to allocate its resources and coordinate the production, distribution, and consumption of goods and services. In essence, an economic system is how a society answers the three questions we discussed earlier.

There are four main types of economic systems: traditional, command, market, and mixed. Each type of economic system has its own unique set of rules and institutions that guide the production, distribution, and consumption of goods and services. For example, a traditional economic system might rely on custom and tradition to guide decision-making, while a command economic system might be characterized by central planning and government control. A market economic system, on the other hand, might be guided by the laws of supply and demand, and a mixed economic system might involve a combination of both market and government decision-making.

In addition to these four types of economic systems, there are also various ways in which an economic system can be evaluated. These include measures of efficiency, equity, and stability. Efficiency refers to the ability of an economic system to produce a large quantity of goods and services with a minimum of resources, while equity refers to the fairness of an economic system in distributing resources and opportunities. Stability, meanwhile, refers to the ability of an economic system to withstand external shocks and maintain a steady state. These ideas are more applicable in a macroeconomics class, but they are ideas that are important to consider when discussing microeconomics as well, since the two are extremely connected!

Types of Economic Systems

Traditional Economies

A traditional economic system is one that is based on custom and tradition. In this type of system, the production, distribution, and consumption of goods and services are guided by cultural norms and values that have been passed down through generations.

In a traditional economic system, the methods of production are often relatively simple and rely on hand tools and basic technology. The division of labor is often based on gender, age, and social status, and there is typically little or no specialization of labor. The distribution of goods and services in a traditional economic system is often based on social and familial relationships. For example, in some traditional societies, land and other resources are passed down through the male line of the family, and wealth and status are inherited. In other traditional societies, resources may be shared more equally among members of the community.

A traditional economic system can be found in societies that have a long history and relatively little contact with the outside world. These societies tend to be relatively isolated and self-sufficient, and they often have a strong sense of community and shared values.

Overall, a traditional economic system is characterized by a reliance on custom and tradition, simple methods of production, and a distribution of goods and services based on social and familial relationships. These systems are a bit rarer in the world compared to command, market, and mixed economies.

Centrally-Planned (Command) Economies

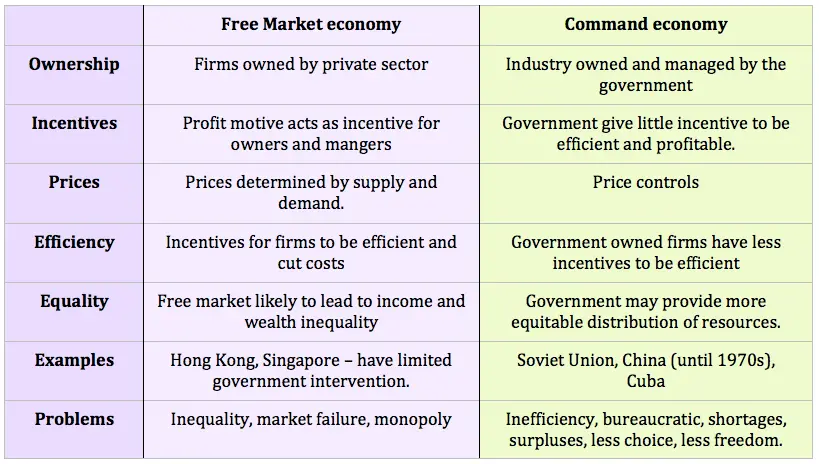

In a command economy, the government or other central authority has complete control over the production, distribution, and consumption of goods and services. The central authority makes all basic economic decisions, including what to produce, how to produce it, and who will receive it. This type of economic system is also known as a planned economy or a socialist economy.

In command economies, the central authority sets production targets and determines how resources should be allocated to meet these targets. It also controls prices and wages, and it may provide certain goods and services for free or at a subsidized price.

One of the main advantages of a command economic system is that it allows the government to direct resources towards important social goals, such as reducing poverty or improving public health. However, this type of system can also be inefficient, as the government may not have access to the same information and incentives as private firms, and it may be more difficult for consumers to express their preferences through the market. This is just one of the trade-offs involved in a command economy. A government may choose to forego economic surplus for social and/or economic control.

Market Economies

A market economy is an economic system in which the production, distribution, and consumption of goods and services are guided by the laws of supply and demand. In a market economy, firms and households are free to buy and sell goods and services, and prices are determined by the forces of supply and demand in a competitive market. Compared to a command economy, a perfect market economy has no central planning body whatsoever. Instead, all answers to the economic questions are left up to the market. This is a topic economist Adam Smith called "the invisible hand."

In a market economy, firms are motivated to produce and sell goods and services that consumers want to buy. To do this, they must find ways to produce efficiently and at a low cost, so that they can offer their products at a competitive price. Consumers, on the other hand, are free to choose which goods and services to buy, based on their preferences and their ability to pay.

One of the main advantages of a market economy is that it allows for the efficient allocation of resources. Because firms are motivated to produce what consumers want to buy, resources are used in a way that reflects the preferences of society. A market economy also allows for innovation, as firms have an incentive to find new and better ways to produce goods and services. However, a market economy also has its drawbacks. One potential disadvantage is that it can lead to income inequality, as those with the resources to invest in businesses or other income-generating assets may earn more than those who do not. A market economy can also be unstable, as prices and demand can fluctuate significantly in response to changes in the economy. In a market economy, efficiency is gained, but without any regulation, can also lead to exploitation, market failure, and externalities.

Mixed Economies

A mixed economy is an economic system that combines elements of both a market economy and a command economy. In a mixed economy, the government plays a role in regulating certain aspects of the economy and providing certain public goods and services, while the private sector is allowed to produce and sell goods and services for profit.

In a mixed economy, the government may intervene in the economy in a number of ways. For example, it may regulate certain industries to protect consumers or the environment, or it may provide public goods and services such as education, healthcare, and infrastructure. The government may also redistribute income through progressive taxation and social welfare programs in order to reduce income inequality.

A mixed economy allows for both the efficiency and innovation of a market economy, as well as the ability to address social goals and address market failures. However, it can also lead to government interference and inefficiencies, as well as conflicts of interest between the public and private sectors.

An example of a mixed economy is the United States. In the US, the government regulates certain industries and provides certain public goods and services, while the private sector is allowed to produce and sell goods and services for profit. The US economy is also characterized by a high degree of income inequality, and the government has implemented progressive taxation and social welfare programs in an attempt to address this issue.

© 2024 Fiveable Inc. All rights reserved.