<< Hide Menu

Jeanne Stansak

dylan_black_2025

Jeanne Stansak

dylan_black_2025

The fundamental topic of economics is scarcity. Scarcity is a fundamental concept in economics that refers to the limited availability of resources in relation to the unlimited wants and needs of individuals and societies. It is the fundamental economic problem of having to choose between alternative uses of limited resources. In other words, scarcity forces us to make trade-offs and choose the most valuable use of our resources. Understanding scarcity and how it affects decision-making is essential to understanding microeconomics, as it helps to explain how individuals and firms allocate resources and make choices about what to produce, how to produce it, and for whom to produce it. This study guide will provide an overview of the concept of scarcity and its role in microeconomics, including how it influences the production and consumption of goods and services, as well as the determination of prices and the allocation of resources in markets.

Scarcity is the basic problem in economics in which society does not have enough resources to produce whatever everyone needs and wants. Scarcity exists because of the idea in economics that all people have infinite wants, but there are limited resources. Scarcity is faced by all societies and economic systems and is inevitable, because we don't have infinite things. As such, scarcity gives rise to the fundamental question of economics: how do we allocate our scarce resources to maximize benefits? This question will guide much of the foundation of economics.

Many students enter an economics class expecting it to be similar to business, but they are two distinct subjects, and scarcity is one of the key differences. Economics and business are often related and overlapping fields, but they are not the same thing. Economics is the study of how societies, households, and individuals allocate their limited resources to satisfy their unlimited wants and needs. It is a social science that deals with the production, distribution, and consumption of goods and services, and it is concerned with the ways in which individuals and societies make choices about how to use their resources.

A diagram of scarcity leading to choices

Scarcity Leads to Choices

Scarcity gives rise to choices because it forces individuals and societies to make trade-offs and decide how to best use their limited resources to satisfy their wants and needs. For example, if an individual only has a limited amount of money to spend, they must choose which goods and services to purchase with that money. They must weigh the costs and benefits of each option and decide which is the most valuable use of their resources. Similarly, if a society has a limited amount of land, it must choose which crops to grow or what industries to develop on that land. It must also decide how to allocate its labor and other resources among these different options. Each of these choices have opportunity costs associated with them, which we'll discuss in detail later. By choosing one thing, we are actively losing another.

In microeconomics, we spend a lot of time understanding the actions of firms, or individual businesses. Scarcity gives rise to choices at the firm level. A firm must decide how to allocate its resources among different production processes, how much to produce, and for whom to produce. For example, a clothing manufacturer must decide how much of its resources to allocate to producing T-shirts versus sweaters, and it must decide how much of each item to produce based on expected demand. These choices are influenced by the prices of inputs and outputs, as well as the firm's goals and objectives.

Overall, scarcity gives rise to choices by forcing individuals, households, firms, and societies to make trade-offs and decide how best to use their limited resources to satisfy their wants and needs.

Opportunity Cost and Trade Offs

Opportunity cost is a key concept in economics that refers to the next best alternative foregone as a result of a decision. It is the cost of an opportunity in terms of the benefits that must be given up in order to pursue it. For example, if an individual decides to go to college, the opportunity cost is the wages they could have earned if they had worked instead of going to school. Opportunity cost is an important concept because it helps to understand the trade-offs that individuals and societies face when making decisions.

It's important to note that opportunity costs don't have to be material. For example, time is a scarce resource that we make choices about all the time. When you opened this study guide, you made an active choice not to say, play video games. Thus, the opportunity cost of studying is the lost fun you would have had playing video games (though I must say, economics is pretty fun too).

Trade-offs, on the other hand, refer to the choices that individuals and societies must make between two or more alternatives. These choices often involve a sacrifice of one thing in exchange for another. For example, a society may face a trade-off between economic growth and environmental protection, as increasing production may lead to pollution and other negative externalities. Similarly, an individual may face a trade-off between leisure time and work, as increasing leisure time may lead to a decrease in income.

In summary, opportunity cost is the cost of an opportunity in terms of the next best alternative foregone, while trade-offs refer to the choices that individuals and societies must make between two or more alternatives, often involving a sacrifice of one thing in exchange for another.

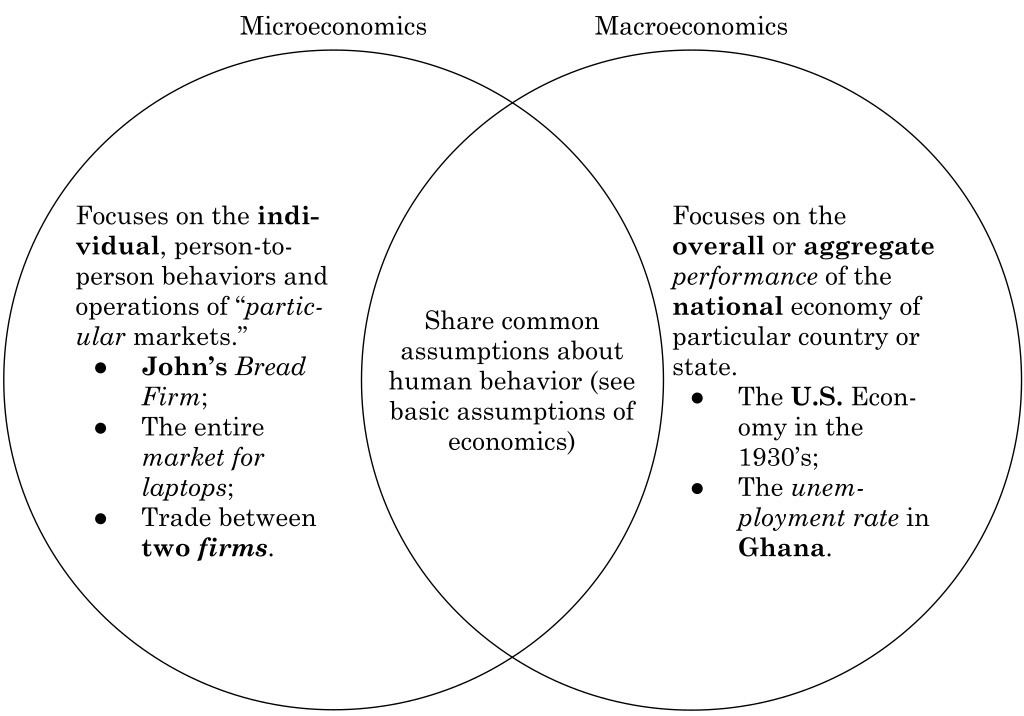

Microeconomics vs. Macroeconomics

While all economists study scarcity and opportunity costs, they split themselves up into microeconomists and macroeconomists. These two fields are the major subfields in economics.

Microeconomics is a branch of economics that focuses on the behavior of individual economic agents, such as households, firms, and consumers. It is concerned with how these agents make decisions and allocate their limited resources to satisfy their wants and needs. A microeconomist may study individual firms or individuals themselves to better understand how scarcity and trade-offs occur on a small level. This involves studying consumer behavior, consumer choice, and producers. For example, some questions a microeconomist may ask is: How does the price of a product affect the quantity of the product that consumers are willing to buy? or how do firms make decisions about what to produce, how to produce it, and for whom to produce it?"

Macroeconomics is concerned with the big picture of the economy, looking at how the overall level of economic activity is determined and how it is affected by changes in policy and other factors. It is a crucial field of study for policymakers and others who are interested in understanding how the economy works and how it can be managed to achieve economic stability and prosperity. A macroeconomist may study how changes in monetary policy, such as an increase in the money supply, affect the level of economic activity and the rate of inflation. They may also study how changes in fiscal policy, such as changes in government spending or tax rates, affect the level of economic activity and the distribution of income. By studying these issues, macroeconomists can gain insights into how the economy operates and how it can be managed to achieve economic stability and growth.

Factors of Production

Factors of Production are the tools we use to produce goods. The resources that are scarce in every society are divided into four categories:

- **Land—**natural resources and raw materials used to make products. Ex: water, vegetation, oil, minerals, and animals. 🚜

- **Labor—**the effort, skills, and abilities that individuals, or employees, devote to a task for which they get paid. 👷

- **Capital—**these types of resources can be divided into two types, physical capital and human capital:

- **Entrepreneurship—**the ability of an individual to coordinate the other categories of resources to invent or produce a good or service. Ex: Bill Gates, Steve Jobs, and Henry Ford. 🚗

Because these resources are scarce, we must choose between them, which brings with it opportunity costs. For example, I could hire thousands of workers on a farm, but that means I might not be able to afford a new tractor.

Examples of Opportunity Costs and Trade-Offs

**Trade-offs—**each of the alternative choices that you gave up when making a decision. For example, you walk into the cafeteria for lunch at school and you have the option of pizza, a cheeseburger, or chicken sandwich for lunch. If you choose to have pizza, then the cheeseburger and chicken sandwich are your trade-offs. 🍕

**Opportunity Cost—**this is the value of the next best alternative when making a choice. Going back to the example of what to have for lunch, if you choose pizza but get to the front of the line and the last slice of pizza was taken by the kid in front of you, you choose a cheeseburger instead. The cheeseburger is your opportunity cost for choosing pizza because it is the next best alternative if your first choice is unavailable. 🍔

| |

© 2024 Fiveable Inc. All rights reserved.